When valuing any business, one of the most important factors to consider is the overall market environment. After all, market conditions have an enormous influence on a company’s performance and what buyers are willing to pay. Privately owned businesses have more protection from immediate market fluctuations than publicly traded companies. But over the longer term, market forces always make their way into financial statements and operational health. In a strong, growing economy, valuations tend to be more generous when demand is high and access to capital is easy. Buyers have more confidence that a target business will continue thriving, allowing them to forecast future solid cash flows. This leads them to place higher multiples on a company’s earnings. Of course, the reverse is true in weaker, uncertain economies as well – buyers become more conservative in their projections, and valuations reflect that uncertainty. Market swings can impact industries and niches very differently, too. For example, a recession may completely deflate valuations of discretionary consumer businesses like gift shops when households pull back spending. As we saw during the result of the pandemic, demand for discount retailers and certain services may remain stable or even grow during downturns. Evaluating the market’s impact requires a nuanced, segment-by-segment analysis in addition to big-picture economic factors. An accurate business valuation must determine how the current market will likely affect future operations. As experts, we analyze historical performance, competitive forces, supplier costs, commodity prices, consumer demand, access to labor, and other external variables that impact […]

Blog

We have distilled decades of experience at the intersection of law, business and finance into a suite of articles to help our clients make sense of business valuation, forensic accounting, and litigation support. Please visit our site regularly for our latest content.

How the Market Impacts Closely-Held Business Valuations

Posted in Business Valuation, on Mar 2024, By: Mark S. Gottlieb

Share

Scrutinizing The Capitalization Rate Within A Business Valuation Report

Posted in Business Valuation, on Feb 2024, By: Mark S. Gottlieb

Share

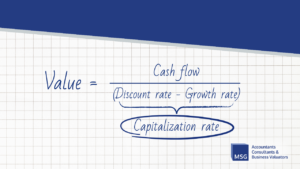

When representing a client with a business valuation report in hand, attorneys must look beyond the numbers at face value. Though you often leave the financial modeling and technical details to the valuation experts, a keen understanding of valuation inputs remains imperative for attorneys on either side of a transaction or dispute. The capitalization rate (a.k.a. the “cap rate”) is among the most impactful business valuation inputs. This factor warrants particular scrutiny, as variations of even 0.5 percent can alter the valuations significantly. Properly vetting this input is essential to achieve an accurate valuation that stands up to legal scrutiny. To add another instrument to your toolbelt, we will provide a quick primer on the cap rate and its components. What is the Capitalization Rate? The capitalization rate is the rate of return used to convert a business’s annual earnings or cash flows into an initial company value, accounting for risk and growth prospects. Computed as the difference between the discount and growth rates, the cap rate involves a nuanced evaluation of multiple factors. Attorneys should be familiar with these items to interpret their credibility quickly. Discount Rate The discount rate is the annual rate used to convert projected future cash flows into present value, reflecting the riskiness, time value of money, and required rate of return an investor would expect on the investment. The most common components used when computing the discount rate are: Risk-free rate of return Equity risk premium Size Premium, and Company-specific risk premium Generally, empirical […]

MSG Adds Three Members to Its Management Team

Posted in News, on Jan 2024, By: Mark S. Gottlieb

Share

NEW YORK, NY – January 22, 2024 -This month, MSG has added three members to its management team, all of whom will be working from its Rockefeller Center headquarters. Renil Thomas James: Manager – Valuation Analyst Renil James is a Certified Financial Analyst chartered by the CFA Institute. Prior to joining MSG, he led valuation teams at Economic Partners and Deloitte Touche. He has vast expertise in the valuation of business enterprises, intellectual property, intangible assets, goodwill impairment testing, & stock options. Lindsey Griffin: Director of Marketing & Client Relations Lindsey Griffin is a seasoned marketing professional. Prior to joining MSG, she was a marketing manager at a multi-disciplined marketing firm. Lindsey will direct the firm’s continued national reach to the legal community while developing and implementing the marketing strategy aligned with the firm’s goals. Reuben Gottlieb: Director of Forensic & Litigation Consulting Reuben Gottlieb is an attorney, certified public accountant, and has earned a master’s degree in forensic accounting. Prior to joining MSG, he has represented private equity firms, public companies, and their portfolio companies in cases involving failed mergers, fraud, and contractual disputes, including cases in the Delaware Chancery Court. _______________________________________________ Mark S. Gottlieb, CPA, PC (MSG) is distinguished as one of New York City and the Tri-State’s premier business valuation, forensic accounting, and litigation support firms. Our practice is devoted exclusively to providing attorneys and their clients with a diverse range of business valuation, forensic accounting, and litigation support services. With over thirty-three years of experience, […]

Detecting ‘Window Dressing’ Tactics in M&A Valuations

Posted in Business Valuation, on Jan 2024, By: Mark S. Gottlieb

Share

As a business valuation expert, I am often called in to assess the true value of a business that is the target of an acquisition. In many such deals, there’s an intricate dance between financial reality and manipulated appearances, which may present a glossier, more appealing image of a company’s financial health than what reality might reveal. In a recently reported case between two private equity firms, the acquirer alleged the seller employed multiple accounting gimmicks to inflate the earnings of a software company, Mobileum, prior to its $915 million sale. By prematurely booking revenues and masking expenses, they claim the target’s profits were artificially inflated by over $250 million. While the allegations remain in dispute, they underscore risks I regularly highlight to clients. As we evaluate the financials of an M&A target, here are some manipulative techniques that our team looks for. Premature Revenue Recognition Illegal yet common, this ploy involves recording future anticipated revenue as current-period income, inflating top-line figures before a sale. Sellers may book forward years of subscription revenue, excessive sales to partners, or less commonly, fictitious sales from shell companies to portray accelerated growth. Capitalizing Expenses This tactic converts regular operating expenses into long-term capital expenditures, enabling costs to be depreciated over years instead of impacting the income statement immediately. By reclassifying expenses as assets without proper documentation, companies reduce reported expenses, inflate reported assets, and subsequently increase profits and net worth. Channel Stuffing A risky tactic, channel stuffing involves shipping surplus products to distributors […]

Changes to Rule 702: An Expert’s Perspective

Posted in News, on Dec 2023, By: Mark S. Gottlieb

Share

The admissibility of expert witness testimony serves as a cornerstone in modern legal proceedings, offering a lens through which complex, specialized knowledge can enlighten the trier of fact. As an expert witness for over 30 years, I have seen the standards for admissibility of expert testimony grow increasingly stringent over time. But who now bears the responsibility of ensuring an expert is fit to serve in that particular legal proceeding? The recent amendment to Rule 702 of the Federal Rules of Evidence, effective as of December 1, 2023, underscores a pivotal shift: elevating the burden of proof on the proponent of the expert witness and amplifying the role of judges in determining admissibility. See below for the amendment: Rule 702. Testimony by expert witnesses. A witness who is qualified as an expert by knowledge, skill, experience, training, or education may testify in the form of an opinion or otherwise if the proponent has demonstrated by a preponderance of the evidence that: a) the expert’s scientific, technical, or other specialized knowledge will help the trier of fact to understand the evidence or to determine a fact in issue b) the testimony is based on sufficient facts or data c) the testimony is the product of reliable principles and methods d) the expert has reliably applied the expert’s opinion reflects a reliable application of the principles and methods to the facts of the case This slight change in verbiage places a much clearer burden on the party offering the expert and makes […]

Mind the GAAP: 10 Basic Generally Accepting Accounting Principles for Attorneys

Posted in News, on Nov 2023, By: Mark S. Gottlieb

Share

“I know nothing about GAAP and I’ll leave it to my accountants.” said Donald Trump Jr. in court yesterday, testifying in the ongoing civil case against former president Donald Trump. GAAP, according to the Financial Accounting Standards Board (FASB), stands for “Generally Accepted Accounting Principles.” GAAP represents a common set of accounting principles, standards, and procedures used in the United States for financial reporting. GAAP encompasses a wide range of rules and guidelines related to accounting, financial reporting, and disclosure. These principles guide how companies prepare their financial statements, including the balance sheet, income statement, and cash flow statement. In litigation cases involving financial fraud or misrepresentation, understanding GAAP requirements provide important context for building and arguing the case. Knowing where GAAP was violated or misapplied can reveal intent and liability. Current principles are based on a number of underlying assumptions. Although these points aren’t codified, they represent generalized assumptions and apply to most financial statements: Regularity – Transactions should be supported by verifiable documentation such as invoices or receipts, ensuring a robust audit trail. Consistency – Consistent accounting treatments and methods must be applied across reporting periods, with any unexplained changes warranting scrutiny. Sincerity – Financial reports must genuinely represent the company’s actual performance and position, avoiding biased estimates and subjective interpretations. Permanence – It is crucial to assume reasonable business continuity rather than liquidation, and any concerns about viability should be thoroughly investigated. Non-Compensation – Assets and liabilities should be treated independently, without offsetting against each other, except […]

How Lower Valuations Can Sweeten the Deal for Employees

Posted in Business Valuation, on Oct 2023, By: Mark S. Gottlieb

Share

Twitter, or “X”, taken private after Elon Musk’s $44 billion acquisition just over a year ago, is now valued at only $19 billion. A new internal memo is cited offering employees restricted stock units (RSUs) at a share price of $45. When private companies offer stock-like compensation options, the IRS advises them to use a 409A valuation – an independent assessment of how much a company is worth. These appraisals tend to be more conservative than valuations based on recent funding rounds or offers from potential acquirers, for example. X itself is “still negative cash flow,” Musk shared in July, citing a “50% drop in advertising revenue plus heavy debt load”. So, it’s not unsurprising that X’s 409A valuation came in lower than the $54.20 per share that Musk paid to take the company private. Because of this conservative approach, it’s common for companies’ 409A valuations to come in lower than their previous private market valuations. Last year, Stripe and Instacart saw their valuations slashed by 28% and 38%, respectively after new 409A appraisals. There are a few reasons why private companies incentivized by employee stock compensation may actually prefer to have lower 409A valuations: Lower strike prices on stock options give employees more potential upside and incentive to join and stay. With a lower valuation, the same number of shares granted or optioned to employees represents less dilution percentage-wise for existing shareholders. Companies can reduce stock-based compensation expenses with a lower 409A valuation. Employees only pay taxes when they […]

Plotting Your Client’s Financial Finish Line: Exits for Entrepreneurial Retirees

Posted in Business Valuation, on Oct 2023, By: Mark S. Gottlieb

Share

As the baby boomer generation continues to reach retirement age, with 10,000 individuals turning 65 every day, the United States is facing a “silver tsunami” of business owners looking to exit their companies. This mass exodus of entrepreneurial talent has made exit planning for retirees an increasingly pressing issue, especially for closely-held businesses. When advising clients on retirement and ownership transition, forensic accountants and business valuators provide invaluable expertise by highlighting crucial financial considerations that can profoundly impact the success of the process. In this blog post, we will explore five key points that business owners should keep top of mind when starting their exit plans. From stock options and business valuations to tax implications and ESOPs, our goal is to provide attorneys and their clients with the financial clarity needed to help navigate the choppy waters of retirement and ownership transition. Stock Options: Stock options are a cornerstone of exit planning. Clients must grasp the significance of these financial instruments, and this is where the expertise of forensic accountants and business valuators becomes crucial. These professionals can elucidate the nuances of restricted stock, stock appreciation rights, and employee stock ownership plans (ESOPs), shedding light on the potential advantages and disadvantages of each option, including intricate details such as control retention and tax implications. Business Valuation: The accuracy of business valuation is paramount in exit planning. Forensic accountants and business valuators possess the specialized skills required to determine the true value of a business. Their expertise in employing diverse valuation […]

Looking Out for Fraud: What Attorneys Need to Know

Posted in Forensic Accounting, on Oct 2023, By: Mark S. Gottlieb

Share

Occupational fraud continues to wreak havoc on businesses, with annual business losses reported to exceed $4.7 trillion worldwide. Fraud experts have long suggested that the presence of three conditions, known as the “fraud triangle,” greatly increases the likelihood that an organization will be defrauded. The classic fraud triangle, as conceived by criminologist Donald Cressey, consists of Pressure, Rationalization, and Opportunity. The Fraud Triangle, Cressey Pressure A perpetrator experiences some type of pressure that motivates fraud. Pressure can come from within the organization – for example, pressure to meet aggressive earnings or revenue growth targets. Alternatively, the pressure could be personal, such as the need to maintain a high standard of living, pay off debt, medical bills, or gambling. Rationalization Perpetrators often mentally justify their fraudulent conduct. They might tell themselves that they’ll pay back the money before anyone misses it, or reason that: They’re underpaid and deserve the stolen funds, Their employers can afford the financial loss, They’ll lose everything (or someone) if they don’t commit fraud, “Everybody” does it, or No other solution or help is available for their problems. Most employees who commit fraud are first-time offenders who don’t view themselves as criminals, but as honest people caught up by circumstances beyond their control. By rationalizing, perpetrators overcome ethical barriers that generally guide their conduct. Opportunity Without opportunity, even motivated and rationalized perpetrators can’t commit fraud. Occupational thieves exploit perceived opportunities that they believe will allow them to go undetected. Weak internal controls, oversight, and auditing create opportunities […]

Legal Consequences of Inflated Valuations: Trump Case and Beyond

Posted in Business Valuation, on Sep 2023, By: Mark S. Gottlieb

Share

Yesterday, New York Supreme Court judge Arthur Engoron ruled in the ongoing lawsuit alleging former President Donald Trump and his businesses provided false financial statements to obtain loans and other benefits. This case piqued my interest as a credentialed business valuation expert, forensic accountant, and expert witness. Yesterday’s decision was over thirty pages long, and I wanted to break down the extent of the document for those following these ongoing legal battles. The New York Attorney General’s office had brought claims against President Trump, his family members, and corporate entities under a statute prohibiting persistent fraudulent conduct in business. The AG submitted evidence that President Trump inflated the valuations of his assets on financial statements from 2011 to 2021. For instance, President Trump claimed his apartment in Trump Tower was 30,000 square feet, later learned to be about three times its actual size. This overstatement led to an overvaluation of over $100 million! The Court also found evidence that other Trump assets, such as branding premiums, shared the same misstatement. President Trump’s legal team asked the Court to dismiss the entire case, arguing the financial statements contained disclaimers and that determining value is subjective. Those requests were later denied. The Court ruled yesterday that the Attorney General provided sufficient evidence that President Trump knowingly submitted false financial statements over multiple years. The judge ordered the dissolution of several corporate entities owned by the Trumps and the appointment of an independent monitor for the Trump Organization. While further potential penalties […]